Budget Tracking

Published by Matthew Turner on

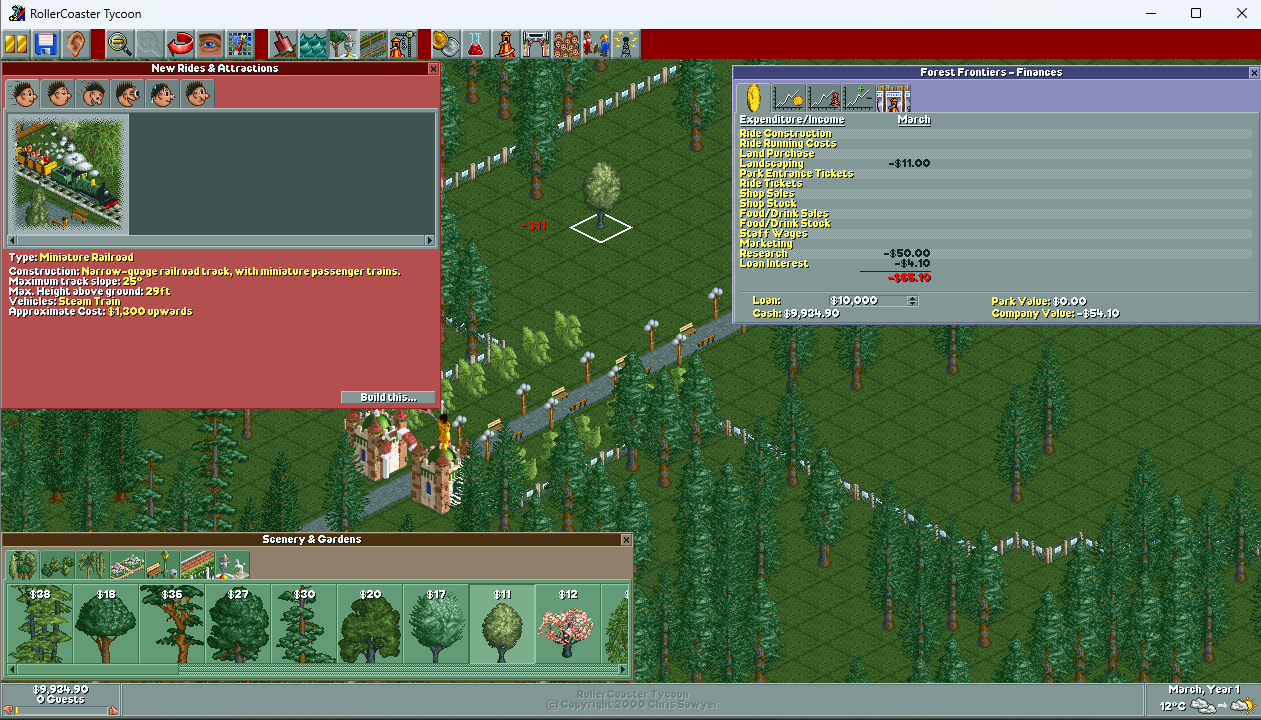

I have been quite annoyed with budgeting software over the last few years. They seem great at first with all of their category flexibility, automatic sync, graphs and analysis, and more. And yet, when I compare them to the original Rollercoaster Tycoon's finance screen, they all fall short.

I loved how the categories matched the menus and how every purchase showed up in real-time, with an added in-world dollar amount floating away to remind you that money was spent. Budgeting software, on the other hand, is wrought with issues. The flexibility of their categories allows for tailoring it to your needs, but what are those needs? There are no starting templates that suggest different options. There is no ability to add descriptions. It is left up to you to understand your own needs and set it up to work for you; something that takes time and a great deal of experience. Sure, “groceries” might seem like an easy category, but do you lump all your medical bills together or separate between medication and massages? What about between children and adults? Then you run into a new issue: any sync, upload, or other capture deals with transactions, but most categories apply to items within transactions. For example, getting diapers during your regular grocery run. Do those really belong into “groceries” (being “food”)? Not really. But then you need to split the transaction with some children's category. Never mind that banks do not allow third-party applications to naturally be granted access—so to have any automatic sync feature you have to hand out your banking credentials verbatim, which is a BIG no-no in terms of security. Then you add on making sure that everything is categorized correctly, keeping an eye on whether you are going over budget, getting distracted by graphs…and it is just too much time managing it.

So I decided to simplify and abandon my Rollercoaster Tycoon benchmark. Instead, the most important distinction I make is between consistent expenses and inconsistent expenses. Consistent expenses are monthly, annual, fixed, or other regularly occurring expenses and purchases (such as restocking groceries); inconsistent expenses are treats, variable costs, exceptional, unexpected, or emergency expenses and purchases (such as a treat at the grocery store). This distinction, in comparison with my monthly income, gives me insight into whether I am actively affording the consistent expenses that I know I will be continuing to spend on (aka, “surviving”), how much this is affected by inflation, and whether there are any suspicious spikes. Once I factor in the inconsistent expenses again, I am less concerned about whether the month-to-month is positive (since events like emergencies are expected to result in a negative one-time spike); and focus, instead, on longer-term trends (is a negative month canceled out by a different positive month?) and whether I have money left over for either free spending or accelerating any savings/investments I set aside (such as replenishing an emergency fund). No more categorization. Just a little bit of management to pull out specific amounts I want to distinguish. Minimal analysis. No budget. Just a super simple spending tracker (demo).